Transfer RRSP from RBC to Questrade was one of the best financial decisions — and I wish I had done it sooner. For years, I kept my RRSP at RBC (Royal Bank of Canada), assuming that a big bank meant safety and convenience. But the more actively I traded, the harder it became to ignore the $9.95 commission charged on every single transaction.

The problem ran even deeper with foreign exchange. Every time I bought U.S. stocks using Canadian dollars, RBC quietly applied a 1.0%–1.45% currency spread. On a $50,000 CAD conversion, that’s CA$725 gone in an instant. And when you later sell those stocks and convert back to CAD, the same cost hits you again. That means a single buy/sell cycle could cost you CA$1,400 or more in FX fees alone — without a single line item ever showing up clearly on your statement.

This guide walks you through exactly how I transferred my RRSP from RBC to Questrade, what it cost, what I got back, and how I now save hundreds of dollars per year using Questrade’s Journaling feature.

1. Why I Decided to Transfer My RRSP Away from RBC

The turning point came from a YouTube video: “BEST Broker in CANADA?” I almost scrolled past it. But when I heard that Questrade charges $0 to buy stocks and ETFs, I had to stop and double-check. After verifying across multiple sources, I confirmed it was true.

RBC vs. Questrade: Side-by-Side Fee Comparison

| Fee Type | RBC Direct Investing | Questrade |

| Trade Stocks | $9.95 / trade | $0 |

| Trade ETFs | 0$ to some ETFs | $0 |

| 10 trades per month | $99.5 | $0 |

| Annual savings | – | Up to $1,194 |

At 10 trades per month, switching to Questrade saves up to $1,194 per year on purchase commissions alone. Compounded inside an RRSP over 30 years, that difference is staggering.

The 2026 Questrade Promotion Sealed the Deal

A limited-time promotion made the decision even easier:

- Open a new account by: April 30, 2026

- Fund your account by: May 31, 2026

- Earn up to: $5,000 cash back depending on transfer amount

Transferring between $50,001 and $100,000 earns a $750 Cash Back bonus. On top of that, Questrade reimburses the transfer fee charged by RBC — up to $150. Effectively, the move costs nothing out of pocket.

2. How to Transfer RRSP from RBC to Questrade — My 4-Step Experience

Many people assume transferring an RRSP is complicated. It isn’t. Here’s the exact process I followed.

Step 1 — Open a Questrade RRSP Account

Visit questrade.com and open an RRSP account online. You’ll need your SIN and a government-issued ID. The process takes about 15– 20 minutes. A helpful walkthrough is available on YouTube: “How to OPEN QUESTRADE Account .”

Step 2 — Submit the Transfer Request

Log in to Questrade and navigate to the Account Transfer section. Enter your RBC account number and the amount you’d like to move. Questrade handles the rest — they contact RBC directly and initiate the transfer on your behalf.

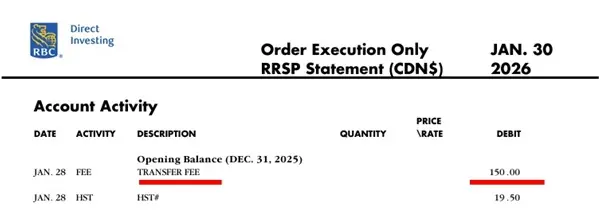

Step 3 — Watch for the RBC Transfer Fee

A few days after submitting the request, RBC charged a $150 transfer-out fee (plus $19.50 HST). Most banks charge this — it’s standard practice. Download the statement showing this charge immediately, as you’ll need it to claim your reimbursement from Questrade.

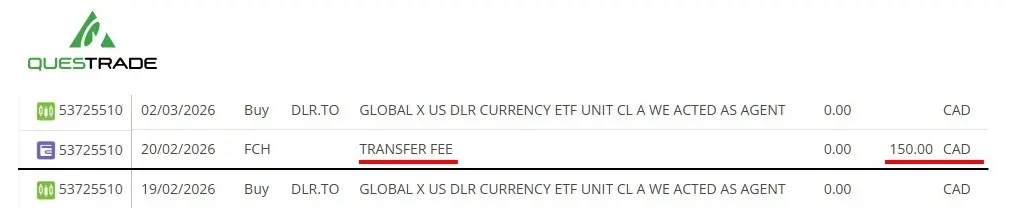

Step 4 — Claim Your Reimbursement from Questrade

Upload the RBC fee statement to Questrade as supporting documentation. In my case, the funds arrived in my Questrade account 12 days after uploading the statement. The $150 fee was fully reimbursed. Note: the $19.50 HST charged by RBC was not reimbursed — only the base transfer fee.

💡 Important: Cash Back Promotion Timeline

The $750 Cash Back is not paid immediately — it differs from the fee reimbursement. Per Questrade support: “The cashback for the promotion starts from June, there will 24 monthly payments for the cashback. You will also receive an email confirmation regarding the expected cashback amount. The email will be in end of May.”

⚠️ Critical Warning: Never Transfer 100% of Your Balance

I made this mistake with a smaller account ($1,200). I transferred the full balance, and RBC automatically closed the account. Once closed, the $150 transfer fee never appeared on any statement — making it impossible to claim the Questrade reimbursement. Questrade requires documentation within 60 days of the transfer date. After multiple email exchanges with RBC Direct Investing, I eventually got the fee waived — but it was stressful. Recommendation: Always leave a small amount (e.g., $100) in the account to keep it open until the fee appears on your statement.

3. Save Even More with Questrade Journaling (Norbert’s Gambit)

After completing the transfer, the feature I became most grateful for was Journaling — Questrade’s implementation of Norbert’s Gambit. It dramatically reduces the cost of converting Canadian dollars to U.S. dollars for investing in U.S. stocks.

| Mothod | Cost on $50,000 CAD | You Save |

| RBC standard FX conversion (1.45%) | CA$725 | – |

| Questrade Journaling | CA$9.95 | CA$715+ |

Across a full buy-and-sell cycle, Journaling reduces your FX cost from CA$1,400+ down to just CA$19.90. Questrade’s official policy: “Journaling is free for Questrade Plus users. A fee of $9.95 per request applies to all other users.”

How to Use Journaling — No Phone Call Required

- Buy DLR.TO (a Canadian-dollar ETF) using your CAD balance

- In Questrade, go to Management Tab → scroll down to “Journal Share” section → submit your request online

- Processing time: officially up to 5 business days — in my experience, about 4 days

- DLR.U.TO (the USD-denominated equivalent) appears in your account automatically

- Sell DLR.U.TO immediately — proceeds settle the same day, giving you USD cash ready to invest

💡 Why Journaling at Questrade Stands Out

Fully self-serve online — no phone call or agent required. Fast and reliable — completed in approximately 4 business days. Far simpler than the process at most other Canadian brokerages. Questrade Plus members pay $0 — the $9.95 fee is waived entirely.

4. What Actually Changed After the Transfer

I transferred between $50,000 and $100,000 in RRSP assets. Here’s my honest assessment after making the switch.

✅ What Got Better

- $0 purchase commissions — I now invest in small, frequent amounts without worrying about fees eating into returns

- Dramatically lower FX costs — Journaling cut my conversion expense from 1.45% to a flat $9.95

- Broader investment options — access to a wider range of ETFs and individual stocks compared to RBC

- $750 Cash Back — paid over 24 months as part of the 2026 promotion

⚠️ What to Watch Out For

- Funds are locked in transit for 15–20 days — plan your timing carefully if you have pending trades

- Questrade’s interface has a learning curve — it’s more feature-rich than RBC’s platform and takes some getting used to

- You cannot sell during Journaling — the shares involved are temporarily locked while the conversion processes

- Never transfer your full balance — always leave a small amount behind to keep the account open

Who Should Make This Switch?

| Great fit ✅ | Think carefully ⚠️ |

| Frequent stock or ETF traders | Investors using only mutual funds (or GIC etc.) |

| Anyone investing in U.S. stocks | Those who prefer in-branch advice |

| Fee-conscious long-term investors | Users unfamiliar with online platforms |

Final Thoughts

Deciding to transfer my RRSP from RBC to Questrade took longer than it should have. Familiarity is comfortable, and change feels risky — especially with retirement savings. But looking back, the process was simpler than I expected, and the financial impact has been real and measurable.

The $9.95 per-trade commission at RBC, the CA$1,400+ per buy/sell cycle in hidden FX costs — these are expenses that silently compound against you over decades of investing. If you hold an RRSP at a major Canadian bank and trade more than a few times a year, running the numbers on a transfer from RBC to Questrade is absolutely worth your time.

I hope this firsthand account helps you make a more informed decision. The math is clear — and so is my experience.

⚠️ Disclaimer

This article is based on the author’s personal experience and is provided for informational purposes only. Investment and financial decisions should always be made in consultation with a qualified financial advisor.

💡 Save Money Beyond Financial Fees: Smart Tech Upgrade Tip!

Just as saving on financial management fees helps grow your wealth, extending the life of your hardware can save hundreds of dollars. Discover how to bypass system requirements and upgrade an older PC to Windows 11 using AI troubleshooting.

👉 Read: How I Saved an Older Desktop with a Windows 11 Upgrade

🌏 한국어 버전으로 읽으시려면 [여기]를 클릭하세요.